The intricate landscape of accounting and tax regulations in Cyprus can be challenging for non-resident companies. At House of Companies, we play a crucial role in assisting foreign companies and individuals with their financial affairs while conducting business in Cyprus. Our services are essential for ensuring compliance with Cypriot tax laws and regulations. From obtaining a VAT number to submitting annual financial statements, we provide comprehensive support to help you fulfill your financial obligations in Cyprus.

In this article, we delve into the key aspects of accounting and tax compliance for non-residents in Cyprus and highlight how House of Companies has revolutionized and simplified Cypriot accounting.

We cover important topics such as corporate income tax, bookkeeping standards, and the benefits of the Cypriot tax regime. By understanding these elements, you can effectively manage your finances and capitalize on opportunities in the Cypriot business environment.

Cypriot Accounting Services: Compliance in Cyprus

Are you a non-resident company looking to navigate the complexities of accounting and tax compliance in Cyprus? Look no further! Our Entity Management Service is here to provide you with the guidance and support you need to ensure your business stays compliant with Cypriot regulations. We understand that dealing with foreign tax laws can be daunting, but with our expertise, you can focus on growing your business while we handle the rest.

Cyprus offers a favorable tax regime with a corporate income tax rate of just 12.5%, one of the lowest in the European Union. However, understanding and complying with local tax laws is crucial. Our team will assist you in obtaining a VAT number, preparing and submitting annual financial statements, and ensuring your corporate income tax obligations are met. We make sure your business is fully compliant, so you can take advantage of the benefits Cyprus has to offer.

Bookkeeping and financial reporting are essential aspects of maintaining compliance in Cyprus. Our experts ensure that your records adhere to International Financial Reporting Standards (IFRS), providing you with accurate and transparent financial statements. We take care of your bookkeeping needs, so you can have peace of mind knowing that your financial records are in good hands.

Most companies in Cyprus are required to have their financial statements audited by a licensed auditor. Our Entity Management Service connects you with experienced local auditors who understand the intricacies of Cypriot regulations. They will ensure that your financial statements are free from material misstatements and comply with all local laws. With our support, you can confidently meet audit requirements and maintain compliance.

Increase your profits with Cypriot Accounting by House of Companies

Are you a non-resident business looking to expand your operations and increase your profits in Cyprus? House of Companies is here to guide you through the complexities of Cypriot accounting and tax regulations. Our entity management service is designed to provide you with the support and expertise you need to navigate the local business environment with confidence.

At House of Companies, we understand that managing your financial affairs in a foreign country can be daunting. That's why our team of experts is dedicated to offering personalized guidance and reassurance every step of the way. From obtaining a VAT number to submitting annual financial statements, we ensure that your business remains compliant with Cypriot tax laws and regulations. Our goal is to help you focus on what you do best – growing your business.

One of the key benefits of partnering with House of Companies is our deep knowledge of the Cypriot tax regime. We help you leverage the favorable tax rates and incentives available to businesses in Cyprus, allowing you to maximize your profits and reduce your tax burden. Our comprehensive bookkeeping and financial reporting services ensure that your records are accurate and up-to-date, giving you peace of mind and enabling you to make informed business decisions.

Don't let the complexities of Cypriot accounting hold you back. With House of Companies by your side, you can confidently expand your business and capitalize on the opportunities that Cyprus has to offer. Contact us today to learn more about our entity management service and how we can help you achieve your business goals.

Overview of Cypriot Accounting Regulations

Understanding the local accounting regulations is crucial for ensuring compliance and optimizing your operations. At House of Companies, we specialize in providing comprehensive entity management services, guiding you through the complexities of Cypriot accounting regulations with ease and confidence.

Cyprus offers a favorable tax regime, with a corporate income tax rate of just 12.5%. However, navigating the intricacies of tax compliance can be daunting. According to Articles 5 and 6 of the Cyprus Income Tax Law, all companies must submit annual tax returns and pay taxes on their worldwide income. Our team at House of Companies helps you understand your obligations, from obtaining a VAT number to submitting annual financial statements, ensuring your business adheres to all local laws.

Bookkeeping and financial reporting in Cyprus must comply with International Financial Reporting Standards (IFRS). This can be challenging for non-resident companies unfamiliar with these standards. Article 33 of the Cyprus Companies Law mandates that all companies maintain proper accounting records and prepare annual financial statements. House of Companies provides expert support to ensure your financial records are accurate and transparent, helping you maintain compliance and build trust with stakeholders.

Most companies in Cyprus are required to have their financial statements audited by a licensed auditor. This includes non-resident entities with significant operations in the country. Article 142 of the Cyprus Companies Law outlines the audit requirements. House of Companies connects you with experienced local auditors who understand Cypriot laws and standards, ensuring your business meets all audit requirements seamlessly.

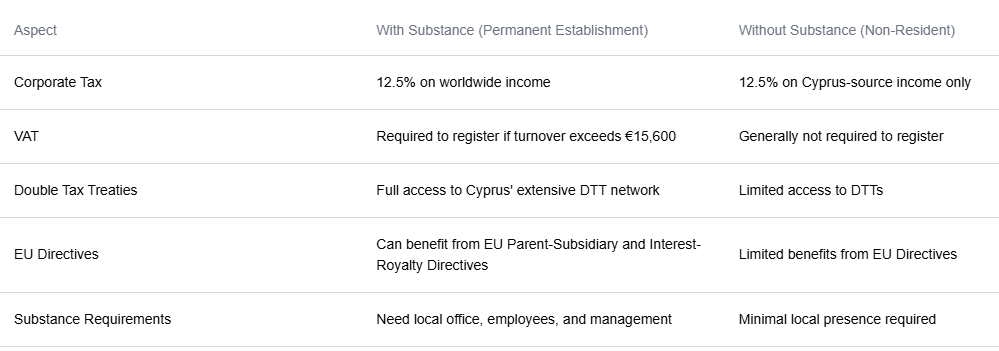

Difference Between a Cypriot Company with Substance (Permanent Establishment) and Without Substance (Non-Resident) for Corporate Tax and VAT

Are you considering establishing a business in Cyprus but unsure about the implications of having a company with substance versus one without? Understanding these differences is crucial for making informed decisions about corporate tax and VAT compliance. At House of Companies, we specialize in providing comprehensive entity management services, guiding you through these complexities with ease and confidence.

A Cypriot company with substance, also known as a Permanent Establishment (PE), is a business that has a physical presence in Cyprus, such as an office or employees. This type of company is subject to corporate income tax at a rate of 12.5% on its worldwide income. Additionally, it must comply with local VAT regulations, which include registering for VAT if engaging in taxable activities. Articles 5 and 6 of the Cyprus Income Tax Law provide detailed guidelines on what constitutes a PE and the associated tax obligations.

On the other hand, a non-resident company without substance in Cyprus is not considered to have a PE. Such companies are only taxed on their income sourced from Cyprus. They are not subject to the same corporate tax rates as resident companies and may have different VAT obligations. According to Article 2 of the Cyprus VAT Law, non-resident companies must register for VAT if they provide taxable supplies within Cyprus, but the compliance requirements can vary.

Choosing the right structure for your business depends on your specific needs and goals. House of Companies provides expert guidance to help you determine whether establishing a company with substance or without substance is the best option for you. We assist with everything from understanding your tax obligations to ensuring compliance with local laws, so you can focus on growing your business.

Legal Entity Types for Non-Residents

Cyprus offers several legal entity types for non-residents, including Limited Liability Companies (LLCs), Branch Offices, and Representative Offices. Each type has its own set of benefits and requirements. Our team at House of Companies helps you choose the right entity type based on your business needs, ensuring compliance with local regulations and optimizing your operations.

Setting up an LLC in Cyprus is a popular choice for many non-residents due to its flexibility and limited liability protection. House of Companies assists you in navigating the registration process, from preparing the necessary documentation to liaising with local authorities. We ensure that your LLC is established smoothly, allowing you to focus on growing your business.

For businesses looking to expand their presence without establishing a separate legal entity, a Branch Office or Representative Office might be the ideal solution. House of Companies provides expert guidance on the specific requirements and benefits of each option, helping you make the best decision for your business. Our entity management services are designed to provide you with the reassurance and support you need to succeed in Cyprus.

At House of Companies, we empower businesses to navigate the Cypriot regulatory landscape with confidence. Our entity management services are tailored to meet the unique needs of non-residents, ensuring a seamless and compliant business setup. Let us help you simplify your entity formation process, so you can focus on achieving your business goals in Cyprus.

Accounting Consequences of Registering a Branch Office in Cyprus

Registering a branch office in Cyprus can be a strategic move for your business, offering numerous benefits such as favorable tax rates and a robust legal framework. However, understanding the accounting consequences is crucial to ensure compliance and maximize these advantages. Our Entity Management Service is here to guide you through every step, providing expert advice and support tailored to your specific needs.

When establishing a branch office in Cyprus, it's essential to be aware of the local accounting standards and reporting requirements. Cyprus follows International Financial Reporting Standards (IFRS), which means your branch will need to prepare financial statements in accordance with these guidelines. Our team will help you navigate these standards, ensuring your financial reporting is accurate and timely, thus avoiding any potential penalties or compliance issues.

Our Entity Management Service offers comprehensive support, from initial registration to ongoing compliance. We understand that managing a branch office can be complex, but with our expertise, you can focus on growing your business while we handle the intricacies of accounting and regulatory requirements. Trust us to provide the reassurance and guidance you need to make your expansion into Cyprus smooth and successful.

Non-resident entities should consult with legal and tax advisors to determine the most suitable option for their specific situation. House of Companies can assist with this in the shape of a corporate plan, for a fixed fee of 295 EUR.

Tax Registration Requirements

Non-resident entities operating in Cyprus must comply with various tax registration requirements to ensure adherence to Cypriot regulations. These obligations may include registering for value-added tax (VAT), payroll taxes, and corporate income tax, depending on the nature and scope of their business activities in the country.

VAT for Businesses with VAT-Taxable Transactions

Businesses engaged in VAT-taxable transactions in Cyprus are required to register for a Cypriot VAT number. This applies to both resident and non-resident companies that supply goods or services (or import) within the country.

The registration process involves submitting an application to the Cyprus Tax Department, providing necessary documentation such as proof of business incorporation and identification documents, and appointing a fiscal representative for non-resident businesses.

House of Companies has automated the process of obtaining a VAT number through our eBranch portal. Once registered, companies must charge VAT on their taxable supplies, file periodic VAT returns, and maintain accurate records of their transactions. The standard VAT rate in Cyprus is 19%, with reduced rates of 5% and 0% applicable to certain goods and services. Non-compliance with VAT obligations can lead to penalties and legal consequences.

Register as Employer When You Payroll Staff in Cyprus

If your business hires employees in Cyprus, you must register as an employer with the Cyprus Tax Department. This registration is essential for fulfilling payroll tax obligations, including the withholding and payment of social insurance contributions and income tax on behalf of your employees.

The registration process involves submitting an employer registration form to the Cyprus Tax Department, along with supporting documentation such as proof of business incorporation and details of your employees. For non-resident businesses, appointing a fiscal representative may be necessary to manage tax matters in Cyprus.

Once registered, you are required to withhold income tax from employee wages, pay both employer and employee social insurance contributions, and report payroll taxes on a monthly basis. Additionally, you must comply with related obligations such as maintaining accurate payroll records and submitting timely tax filings.

Failure to register as an employer and comply with payroll tax obligations can result in penalties, interest on unpaid taxes, and potential legal issues. To navigate this process efficiently and ensure full compliance with Cyprus tax law, our House of Companies can assist you with employer registration, payroll management, and ongoing compliance, offering professional guidance every step of the way.

Corporate Tax Liability for Resident Companies

Understanding corporate tax liability is crucial for resident companies aiming to maintain compliance and optimize their financial strategies. In Cyprus, resident companies are subject to a corporate tax rate of 12.5% on their worldwide income.

This competitive rate, along with various tax incentives, makes Cyprus an attractive destination for businesses. Our Entity Management Service provides comprehensive support to ensure your company meets all tax obligations efficiently.

Our team of experts will guide you through the intricacies of Cypriot tax laws, helping you leverage available deductions and credits to minimize your tax burden.

We assist with accurate tax filings, timely payments, and strategic planning to align your tax strategy with your business goals. With our proactive approach, you can avoid penalties and make informed decisions that enhance your company's profitability.

Bookkeeping and Financial Reporting

Effective bookkeeping and financial reporting are essential for maintaining the financial health and compliance of your business. Accurate bookkeeping ensures that all financial transactions are recorded systematically, providing a clear picture of your company's financial status. Our Entity Management Service offers meticulous bookkeeping solutions, tailored to your business needs, ensuring that your financial records are always up-to-date and accurate.

Financial reporting goes hand-in-hand with bookkeeping, providing insights into your company's performance and aiding in strategic decision-making. Our team of experts prepares comprehensive financial reports, including balance sheets, income statements, and cash flow statements. These reports not only help you understand your financial position but also ensure compliance with regulatory requirements. With our support, you can confidently present your financial data to stakeholders and regulatory bodies.

Partnering with our Entity Management Service means you can focus on growing your business while we handle the complexities of bookkeeping and financial reporting. We provide personalized guidance, helping you navigate financial regulations and optimize your financial strategies. Trust us to keep your financial records in order, so you can make informed decisions and drive your business forward.

Tip: No Need to Register a Local Company in Cyprus for Payroll Tax Compliance You don't need to set up a local company or branch office in Cyprus to comply with payroll tax regulations, unless you employ staff directly in the country or outsource staff to third parties. In those cases, you must meet specific payroll tax and social insurance obligations.

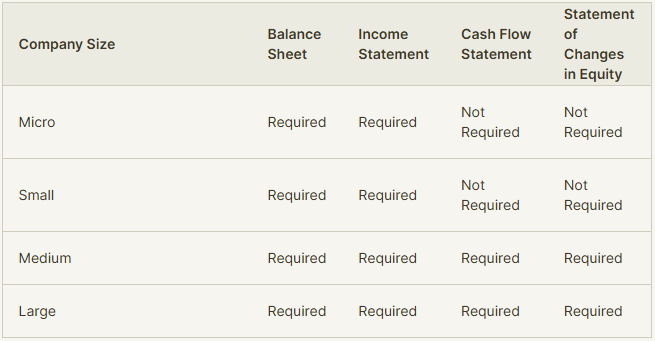

Content of Financial Statements

The principal of financial statements in Cyprus is to provide a true and fair view of a company's financial position and performance. These statements must comply with International Financial Reporting Standards (IFRS) and include key documents such as:

Balance sheet

Income statement

Cash flow statement

Statement of changes in equity.

Additionally, they must be prepared with transparency and accuracy, ensuring that all financial activities are clearly documented and disclosed. This practice not only aids in regulatory compliance but also enhances the trust and confidence of investors, stakeholders, and regulatory bodies in the financial health and integrity of the company.

Consolidation Requirements

In Cyprus, companies that are part of a group may be required to prepare consolidated financial statements. Consolidation involves combining the financial statements of the parent company with those of its subsidiaries to present a single set of financial statements for the entire group.

The requirement to consolidate financial statements typically applies to companies that have control over one or more subsidiaries. Control is generally defined as having more than 50% of the voting rights or the ability to govern the financial and operating policies of the subsidiary.

Consolidated financial statements must include a balance sheet, income statement, statement of changes in equity, cash flow statement, and notes to the financial statements. These statements should be prepared in accordance with International Financial Reporting Standards (IFRS) as adopted by the European Union.

There are certain exemptions available for small and medium-sized groups, which may not be required to prepare consolidated financial statements if they meet specific criteria related to size and turnover. However, even if exempt, companies may choose to prepare consolidated statements for transparency and better financial reporting.

Non-compliance with consolidation requirements can result in penalties and affect the credibility of the financial statements. Therefore, it is crucial for companies to understand their obligations and ensure proper consolidation of their financial records.

Audit Requirements

In Cyprus, companies are generally required to have their financial statements audited by a licensed auditor. The audit ensures that the financial statements provide a true and fair view of the company's financial position and comply with International Financial Reporting Standards (IFRS).

Certain small and medium-sized enterprises (SMEs) may be exempt from mandatory audits if they meet specific criteria related to turnover, total assets, and number of employees. However, even exempt companies may choose to undergo an audit for transparency and credibility.

Non-compliance with audit requirements can result in penalties and affect the company's reputation. It is crucial for businesses to understand their audit obligations and ensure timely compliance.

Publication Requirements

The financial statements must be prepared and approved by the managing directors no later than five months after the end of the financial year, with a possible extension of up to five months. The publication requirements vary depending on the company's size, as summarized in the table below:

Non-resident entities must comply with bookkeeping and financial reporting requirements to ensure adherence to Cypriot regulations and maintain transparency in their business operations.

Annual Accounts Filing Obligations

companies are required to prepare and file annual accounts to ensure transparency and compliance with local regulations. These accounts must be prepared in accordance with International Financial Reporting Standards (IFRS) and include the balance sheet, income statement, cash flow statement, and notes to the financial statements.

The annual accounts must be submitted to the Registrar of Companies within 12 months from the end of the financial year. Public companies and certain private companies are also required to publish their financial statements in the Official Gazette of Cyprus.

Non-compliance with filing obligations can result in penalties and legal consequences. It is crucial for companies to adhere to these requirements to maintain compliance and credibility.

Audit Requirements

In Cyprus, most companies are required to have their financial statements audited by a licensed auditor. This audit ensures that the financial statements provide a true and fair view of the company's financial position and comply with International Financial Reporting Standards (IFRS). The audit process involves a thorough examination of the company's financial records, internal controls, and accounting practices to verify the accuracy and completeness of the financial statements.

Certain small and medium-sized enterprises (SMEs) may be exempt from mandatory audits if they meet specific criteria related to turnover, total assets, and the number of employees. However, even exempt companies may choose to undergo an audit for transparency and credibility. Non-compliance with audit requirements can result in penalties and affect the company's reputation. It is crucial for businesses to understand their audit obligations and ensure timely compliance to maintain trust with stakeholders and regulatory authorities.

Audit Requirements for Non-Resident Entities

Non-resident entities operating in Cyprus must adhere to specific audit requirements to ensure compliance with local regulations. These requirements vary depending on the size and nature of the business activities conducted within the country.

Non-resident entities are generally required to undergo an audit if their annual turnover exceeds certain thresholds set by Cypriot law. The audit must be conducted by a licensed auditor or audit firm registered in Cyprus. The primary objective of the audit is to verify the accuracy and completeness of the financial statements and ensure they comply with Cypriot accounting standards and regulations.

The audit process involves a thorough examination of the entity's financial records, transactions, and internal controls. The auditor will assess the financial statements to ensure they provide a true and fair view of the entity's financial position and performance. This includes verifying the accuracy of revenue, expenses, assets, and liabilities reported in the financial statements.

In addition to the financial audit, non-resident entities may also be subject to compliance audits. These audits focus on ensuring that the entity adheres to all relevant tax laws, employment regulations, and other legal requirements in Cyprus.

Failure to comply with audit requirements can result in penalties and legal consequences. It is essential for non-resident entities to understand their audit obligations and engage a qualified auditor to conduct the necessary audits. This ensures transparency, accuracy, and compliance with Cypriot regulations, thereby avoiding potential legal issues and maintaining the entity's reputation.

VAT Compliance for Foreign Businesses

Foreign businesses operating in Cyprus must comply with Cypriot VAT regulations, which are governed by the Cyprus VAT Law and the EU VAT Directive. Non-resident entities must register for VAT if they are conducting taxable transactions within Cyprus or if they meet certain thresholds.

Non-resident companies can choose to become a resident for VAT purposes by establishing a local office or hiring local employees. By doing so, they simplify VAT compliance, as it allows for the submission of monthly VAT returns and the ability to appoint a fiscal representative in Cyprus to handle VAT matters.

Alternatively, non-resident companies can maintain their non-resident status and take advantage of the Art. 23 exemption, which allows for the deferral of import VAT payments. However, this exemption comes with additional administrative requirements, including the obligation to file quarterly VAT returns.

Another option for foreign businesses is to use bonded warehouses. Goods stored in a bonded warehouse are not subject to VAT or customs duties until they are released for circulation within the EU. This can provide businesses with significant cash flow benefits and flexibility in managing their supply chain.

To use a bonded warehouse in Cyprus, businesses must obtain a permit from the Cyprus Customs Authorities. The permit holder is responsible for maintaining accurate records of the goods, such as product codes, customs value, country of origin, weight, and measurements.

While goods in a bonded warehouse cannot be processed or altered, certain value-added services, such as repackaging, quality control, and labeling, can be performed to keep the goods in good condition or prepare them for distribution.

Once goods are released from the bonded warehouse and enter circulation within Cyprus or the EU, VAT and excise duties become due. The deferred VAT and duties must be paid in the country where the goods are released, unless a customs transport permit (T1 document) is obtained for shipment to another EU member state.

Cypriot GAAP vs IFRS Reporting Standards

Understanding the differences between Cypriot Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) is crucial for businesses operating in Cyprus. Both frameworks aim to ensure transparency and consistency in financial reporting, but they have distinct characteristics and requirements.

Cypriot GAAP Cypriot GAAP is the local accounting standard used by companies operating within Cyprus. It is based on the European Union's accounting directives and incorporates specific local regulations and practices. Key features of Cypriot GAAP include:

Historical Cost Principle: Assets and liabilities are generally recorded at their historical cost.

Prudence Principle: Emphasizes caution in financial reporting, ensuring that liabilities and expenses are not understated, and assets and income are not overstated.

Consistency Principle: Requires companies to apply the same accounting methods and principles from one period to the next to ensure comparability.

IFRS IFRS is a globally recognized set of accounting standards developed by the International Accounting Standards Board (IASB). It is designed to bring consistency and comparability to financial statements across international borders. Key features of IFRS include:

Fair Value Measurement: Assets and liabilities are often measured at their fair value, providing a more current valuation.

Principle-Based Approach: IFRS focuses on the principles behind the transactions rather than detailed rules, allowing for more flexibility and professional judgment.

Global Consistency: Ensures that financial statements are comparable across different countries, facilitating international investment and business operations.

Key Differences

Measurement of Assets and Liabilities: Cypriot GAAP typically uses historical cost, while IFRS often employs fair value measurement.

Revenue Recognition: IFRS has specific standards for revenue recognition (IFRS 15), which may differ from the principles under Cypriot GAAP.

Financial Statement Presentation: The format and presentation of financial statements can vary, with IFRS requiring a statement of changes in equity, which may not be mandatory under Cypriot GAAP.

Disclosure Requirements: IFRS generally requires more extensive disclosures in the financial statements compared to Cypriot GAAP.

Transitioning from Cypriot GAAP to IFRS For companies transitioning from Cypriot GAAP to IFRS, it is essential to understand the differences and adjust their accounting policies and procedures accordingly. This may involve revaluating assets and liabilities, changing revenue recognition practices, and enhancing financial statement disclosures.

By understanding and applying the appropriate accounting standards, businesses can ensure compliance and provide accurate and comparable financial information to stakeholders.

Receiving or Paying Dividends to or from Your Group Company

Dividends from Cypriot resident corporations are generally subject to a 17% dividend withholding tax (WHT), as per Cyprus tax law. However, dividends may be exempt from this withholding tax under specific conditions. The exemption typically applies if the recipient of the dividends is a resident of the European Union, the European Economic Area, or another jurisdiction with which Cyprus has concluded a tax treaty that includes a dividend article, provided that anti-abuse provisions are not triggered.

No Withholding Tax Consequences for a Branch Office

A foreign company with a branch in Cyprus is not required to prepare its own Cypriot financial statements, although a stand-alone balance sheet and profit and loss account may be necessary for tax purposes. Since a branch is not considered a separate legal entity, there are no withholding tax consequences for transactions between the head office and the branch.

How to Represent a Subsidiary on Your Cypriot Balance Sheet

Parent companies should generally consolidate the financial data of "controlled subsidiaries" and other "group companies" in their consolidated financial statements. Under Cypriot law, a "controlled subsidiary" is a legal entity in which the company can directly or indirectly exercise more than 50% of the voting rights at the shareholders' meeting or has the authority to appoint or dismiss the majority of the managing or supervisory directors (Cyprus Companies Law, Cap. 113, Section 4).

How to Represent a Subsidiary on Your Cypriot Balance Sheet

Parent companies should generally consolidate the financial data of "controlled subsidiaries" and other "group companies" in their consolidated financial statements. Under Cypriot law, a "controlled subsidiary" is a legal entity in which the company can directly or indirectly exercise more than 50% of the voting rights at the shareholders' meeting or has the authority to appoint or dismiss the majority of the managing or supervisory directors (Cyprus Companies Law, Cap. 113, Section 4).

Process Incoming or Outgoing Dividend Payments on Your Balance Sheet

Incoming dividend payments received from a subsidiary should be recorded as financial income in the parent company's profit and loss account. A corresponding receivable should be recorded on the balance sheet until the payment is received.

Outgoing dividend payments to shareholders should be recorded as a reduction in retained earnings on the balance sheet, with a corresponding liability recorded until the payment is made.

Annual Reporting Deadlines and Requirements

Cypriot companies are required to submit their annual financial statements and reports to the Registrar of Companies and the Tax Department. The annual return (HE32) must be filed within 42 days from the company's annual general meeting (AGM), which should be held within 15 months of the previous AGM. Financial statements must be prepared in accordance with International Financial Reporting Standards (IFRS).

Filing Requirements

Companies must file the following documents annually:

Annual Return (HE32): Includes details of the company's directors, shareholders, and registered office.

Financial Statements: Must be audited and include the balance sheet, income statement, and notes to the financial statements.

Tax Return: Must be submitted to the Tax Department, along with the audited financial statements.

Penalties for Non-Compliance

Failure to comply with annual reporting and filing requirements can result in significant penalties, including:

Late Filing Fees: Penalties for late submission of the annual return and financial statements.

Fines: Additional fines may be imposed for non-compliance with statutory requirements.

Legal Consequences: Persistent non-compliance can lead to legal actions, including the striking off of the company from the Registrar of Companies.

Audit Thresholds for Cypriot Companies

Failure to comply with annual reporting and filing requirements can result in significant penalties, including:

Late Filing Fees: Penalties for late submission of the annual return and financial statements.

Fines: Additional fines may be imposed for non-compliance with statutory requirements.

Legal Consequences: Persistent non-compliance can lead to legal actions, including the striking off of the company from the Registrar of Companies.

Cyprus Company Size Classification

Note: Companies are classified based on meeting at least two of the three criteria (Assets, Turnover, Employees) for their respective size category.

Audit Thresholds for Cypriot Companies

For SMEs that meet the exemption criteria, there is no requirement to have their financial statements audited by a chartered accountant. These businesses can prepare unaudited financial statements, which must still comply with IFRS and be submitted to the relevant authorities. This exemption helps reduce the administrative and financial burden on small businesses.

FAQs

1. What are the annual reporting deadlines for Cypriot companies?

Cypriot companies must submit their annual financial statements and reports to the Registrar of Companies and the Tax Department. The annual return (HE32) must be filed within 42 days from the company's annual general meeting (AGM), which should be held within 15 months of the previous AGM.

2. What are the filing requirements for Cypriot companies?

Companies must file the following documents annually:

Annual Return (HE32): Includes details of the company's directors, shareholders, and registered office.

Financial Statements: Must be audited and include the balance sheet, income statement, and notes to the financial statements.

Tax Return: Must be submitted to the Tax Department, along with the audited financial statements.

3. What are the penalties for non-compliance with annual reporting requirements?

Failure to comply with annual reporting and filing requirements can result in significant penalties, including late filing fees, fines, and potential legal consequences such as the striking off of the company from the Registrar of Companies.

4. What are the audit thresholds for Cypriot companies?

Small and medium-sized enterprises (SMEs) may be exempt from the audit requirement if they meet two of the following three criteria:

Turnover: Less than €700,000.

Total Assets: Less than €1,000,000.

Employees: Fewer than 10 employees.

5. Is a chartered accountant or audit required for SME businesses in Cyprus?

For SMEs that meet the exemption criteria, there is no requirement to have their financial statements audited by a chartered accountant. These businesses can prepare unaudited financial statements, which must still comply with IFRS and be submitted to the relevant authorities.

Wherever I pay tax, that’s my home.

Feel welcome, and try out our solutions and community, to bring your business a step closer to international expansion.